{kind=link}

Before Fall Move-In, Check What a Renters Policy Still Leaves Out

A lot of students and young renters buy a policy in ten minutes, upload the proof to the landlord portal, and assume the job is done. That can work for lease compliance, but it does not always protect the laptop, bike, borrowed electronics, or liability risk that matter most once classes start and boxes are piled into a new place.

This late-summer review is different from a general back-to-campus shopping checklist. The real issue is whether a renters policy fits the way student housing actually works: roommates, shared entryways, older buildings, water mishaps, package theft, and a tight budget that makes even a modest uncovered loss painful.

Before the first September rent payment and before a move-in scramble, it helps to compare more than the monthly premium. A cheap policy can still leave big holes if the deductible is too high, the personal property limit is too low, or key situations are excluded. The good starting point is the official consumer insurance guidance in your state, plus a careful read of what a standard renters policy does and does not include. The renters coverage basics from the NAIC and the common coverage outline from the Insurance Information Institute can help frame the comparison.

Cheap proof for the landlord is not the same as useful protection

The first trap is buying the lowest-price policy only because the lease requires one.

A policy that satisfies a landlord’s upload requirement may still be a weak match for the belongings and risks inside the unit.

Many lease agreements ask for renters insurance, but they often set only a minimum liability amount and say little about your personal property. That means a student can meet the building rule with a bare-bones policy and still be underinsured from day one. If a bedroom contains a computer, tablet, headphones, textbooks, gaming gear, clothing, and a bike, replacement costs can rise quickly. Yet many renters underestimate the total because they think item by item instead of room by room.

Start with three numbers: personal property coverage, liability coverage, and deductible. Then compare them against real life. If the deductible is $1,000 and the likely loss is a $1,200 stolen laptop plus a few smaller items, the policy may not help much. If liability coverage is the minimum required by the landlord, ask whether that still feels enough if a kitchen fire, bathtub overflow, or dog bite claim affects someone else.

It also helps to ask whether the policy pays replacement cost or actual cash value for belongings. That difference can shape how much comes back after a claim.

Use a quick room-based inventory before you shop:

- School and work electronics

- Clothing and shoes

- Furniture and bedding

- Sports gear or instruments

- Kitchen items and small appliances

- Bikes, scooters, or parking-lot items

A short phone video of the room can also help later if you need to document what you owned.

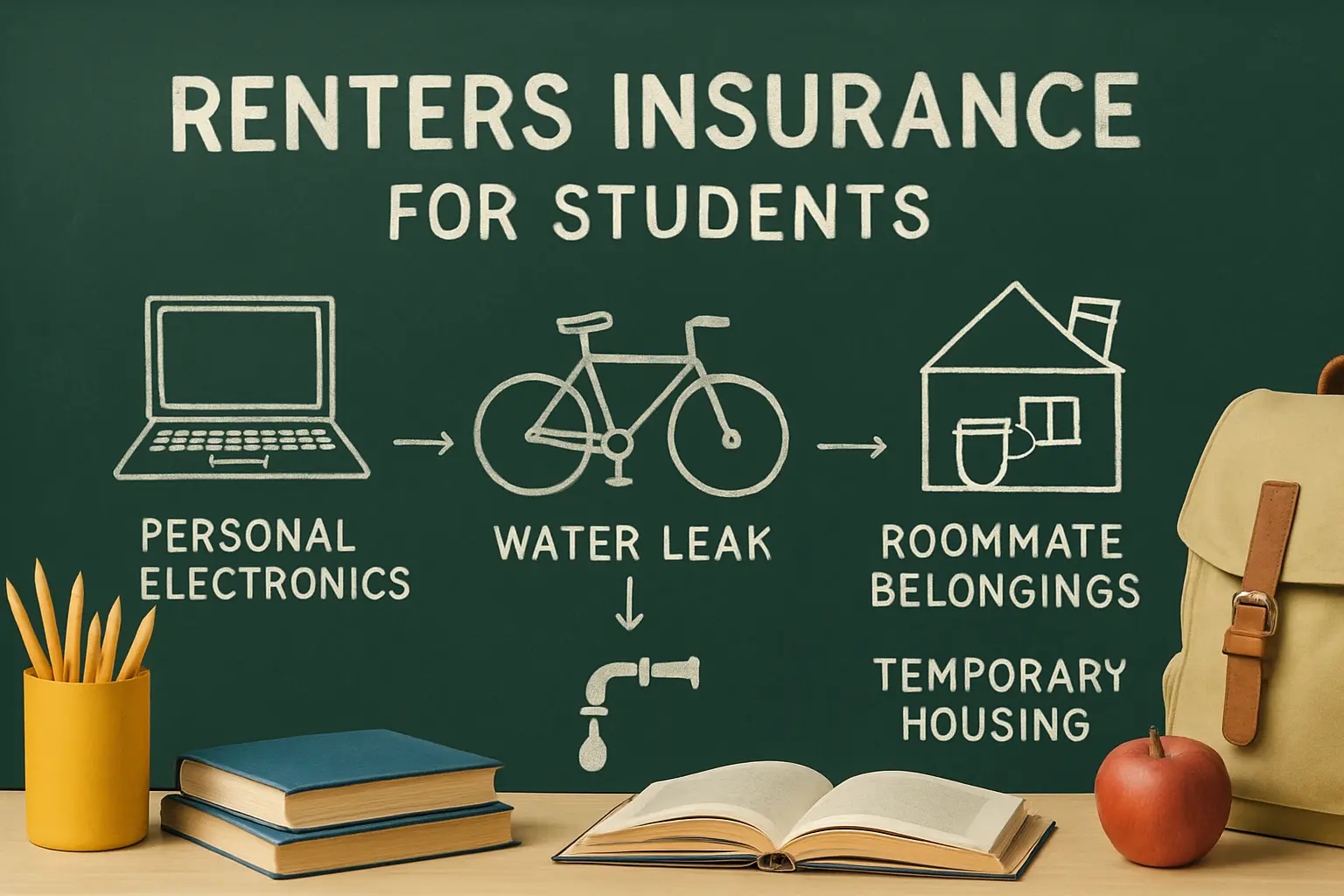

Water, theft, and roommate issues create the most surprise gaps

The biggest misunderstandings usually show up around what caused the loss and who owned the damaged property.

Two losses that feel almost identical to a renter can be treated very differently depending on whether the cause was a burst pipe, a backup, a flood, or another person’s property.

Standard renters coverage often helps with certain sudden events, but not every wet mess or theft claim works the same way. Water from a burst pipe may be treated differently from sewer or drain backup, and flooding from outside is commonly a separate issue. That is why students in basement units, older houses, or storm-prone areas should ask about exclusions before choosing only on price. The federal flood insurance program is worth a look if outside water is a realistic risk.

Theft also gets messy in student housing. A stolen package from the lobby, a bike taken from a rack, or electronics disappearing from a shared space may involve different claim questions than a clean break-in. Some policies place tighter limits on property used away from the home or stored in common areas.

Then there is the roommate issue. One renter’s policy usually does not automatically cover another unrelated roommate’s belongings. If each person wants protection for their own property, each may need separate coverage unless the insurer explicitly allows a shared arrangement. That rule is easy to miss in off-campus houses and dorm-style apartments.

Ask these direct questions before buying:

- Does this cover belongings stolen away from the unit?

- Are bikes or scooters subject to lower limits?

- Is water backup excluded unless added?

- Does the policy cover only my property, or a roommate’s too?

- Are packages and items in shared areas treated differently?

The clearer these answers are up front, the less likely a fall-semester claim becomes an ugly surprise.

Small add-ons can matter more than a flashy discount

Endorsements and optional features are often where a student policy becomes either useful or flimsy.

A slightly higher premium can be the better value when it closes one realistic gap that would otherwise cost hundreds or thousands after a loss.

Many renters never look at add-ons because they assume endorsements are for expensive homeowners policies. In practice, a few optional protections can matter a lot in student housing. Water backup coverage may be worth reviewing in older buildings. Scheduled personal property can help if you own a high-end bike, musical instrument, camera, or jewelry that exceeds the usual category limit. Identity theft support may also appeal to people whose school and banking life runs almost entirely online.

Another feature worth checking is loss-of-use coverage, sometimes called additional living expenses. If a fire, major leak, or other covered event makes the apartment unlivable during the semester, this part of the policy may help with hotel or temporary housing costs. In a college town during fall move-in season, that can matter more than people expect.

Look at each quote side by side for:

- Water backup option

- Extra coverage for valuables

- Replacement cost on belongings

- Identity theft or fraud assistance

- Loss-of-use limit

- Pet liability rules if a pet is in the unit

This is also a good moment to compare bundle discounts carefully. Saving money by pairing auto and renters coverage can be helpful, but the coverage itself still has to fit. A bundle is not a bargain if the renters side has the wrong deductible or missing protection.

For families helping a student pay bills, this can also be a place to compare whether a dependent’s belongings are already protected under another policy in limited situations. That is not something to assume. It is something to confirm in writing with the insurer.

State rules and campus housing details can change what matters most

Your state insurance department and your lease terms may reveal practical limits that ads never mention.

The fine print that matters most is often local: how claims are regulated in your state, what the lease requires, and whether the building setup creates special risks.

Insurance is regulated at the state level, so the smartest place to verify basic rights and complaint channels is your state insurance department. The state insurance department directory can help you find the right office. These sites often explain consumer protections, complaint steps, and policy terms in plain language.

Your lease matters too. Some landlords require only liability coverage. Others require proof by a specific move-in date, list the landlord as an interested party, or impose deadlines for maintaining coverage. Student-focused housing may also have rules about waterbeds, pets, balcony storage, or certain risks that affect liability.

Check local details like:

- Whether the building has a history of leaks or backups

- Whether bikes are stored inside or outside

- Whether packages pile up in an unsecured mail area

- Whether the unit is in a basement or lower floor

- Whether unrelated roommates each need separate proof

Campus-area apartments also turn over fast. If you are moving from a dorm to an off-campus unit, update the address and property setup right away. A policy tied to the old location may not fit the new one, and address mistakes can create claim headaches later. This is one of those routine admin tasks that is boring until it matters.

In short, state guidance helps with the rules, but the lease and building tell you what your real risks look like once the semester begins.

Use a one-week move-in insurance check before classes start

A short review now can help you buy the right policy before the apartment gets crowded and deadlines get missed.

The easiest renters insurance savings usually come from choosing the right fit once, not from chasing the absolute lowest premium and fixing mistakes after a claim.

Keep the process simple and practical. On day one, make a rough inventory and total the value of your belongings. On day two, pull your lease and note the required liability amount and proof deadline. On day three, get at least two or three quotes with the same limits so you can compare clearly. On day four, check whether replacement cost, water backup, or scheduled property add-ons make sense. On day five, confirm the final policy details, upload proof if needed, and save the declarations page somewhere easy to find.

A good final checklist looks like this:

- Count the value of what is actually in the unit

- Match liability coverage to the lease and your comfort level

- Choose a deductible you could realistically pay

- Check theft, water, and roommate-related limits

- Review add-ons for bikes, instruments, valuables, or backup risk

- Save your inventory video and policy documents

- Verify your state insurance department contact page

Renters insurance works best when it is treated like protection, not just paperwork. Before fall leases settle in and class schedules take over, take a few minutes to compare what your policy really covers and which gaps may still need attention today.