{kind=link}

Could Your Renters Policy Still Miss Key Losses This July?

A renter pays for a policy, assumes the basics are handled, and only learns about the holes after a leak, theft, or temporary move-out. That is why July is a smart time to look at renters insurance updates with fresh eyes. The question is not only whether prices changed. It is whether the weak spots in a typical policy are getting better in your state, or whether the same old exclusions are still sitting there waiting to surprise you.

Across the country, insurance markets are still shifting. In California, for example, a settlement tied to State Farm’s earlier emergency rate request shows how regulators and insurers are still wrestling with affordability and market stability. That does not directly rewrite every renters policy, but it is a reminder that state-level insurance conditions can affect cost, availability, and how carefully renters need to compare options. At the same time, general 2026 coverage guides from sources reviewing apartment renters insurance basics and current renters insurance rates keep pointing to the same reality: many renters remain underinsured not because they skipped coverage, but because they never checked what was missing.

Instead of treating this like a pure insurance-news story, the useful move is to run a short midyear review. A few careful checks can help you spot whether your current policy still leaves out the losses most likely to hurt your budget.

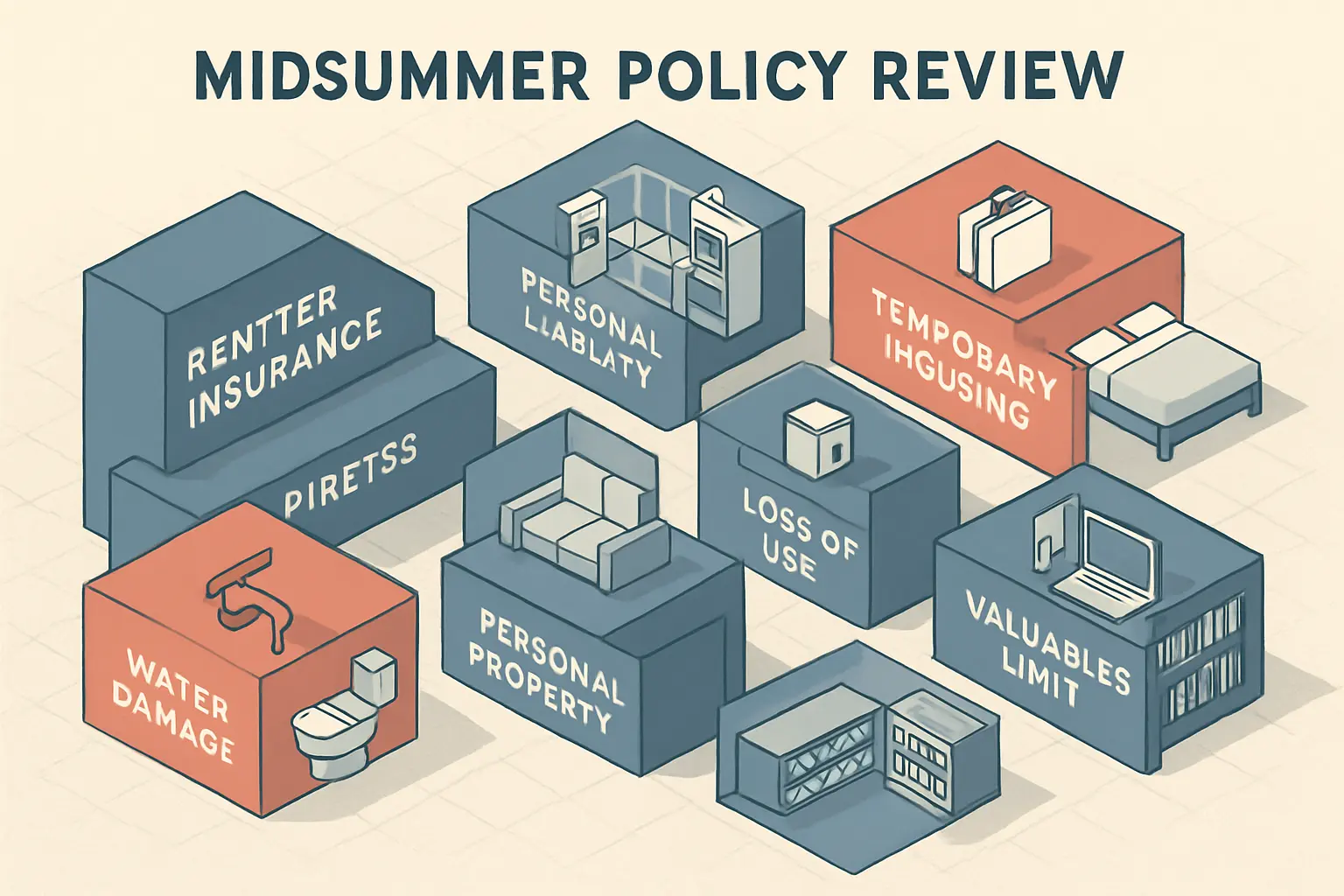

Where renters usually discover the biggest holes

The riskiest gap is often not having no insurance at all; it is having a policy that covers less than you think.

Many renters learn too late that a standard policy can be solid for some losses and still weak on water damage, high-value items, temporary housing details, or liability limits.

Start with the weak areas that show up over and over in renters coverage. A basic policy often includes personal property, liability, and some loss-of-use protection, but that does not mean every common apartment problem is covered the same way. Water is a classic example. Sudden damage from a burst pipe may be handled very differently from flooding, sewer backup, or slow leaks. Jewelry, bikes, instruments, collectibles, and work equipment can also have tight limits unless you add extra protection. Even temporary housing coverage can be narrower than renters expect if the policy only pays for certain causes of loss or has lower dollar caps than your local rental market would suggest.

That is why a July review should focus less on the monthly premium and more on the real pressure points. Pull out your declarations page and ask:

- What is the personal property limit, and would it actually replace your belongings?

- What events are excluded, especially flood and backup-related losses?

- What is the liability amount if someone gets hurt in your unit?

- How much would the policy pay if you had to live elsewhere for a few weeks?

- Are there category caps for electronics, jewelry, bikes, or specialty items?

Guides such as the 2026 renters insurance overview keep stressing that many policies look similar until you read the sublimits and exclusions. That matters most for renters in apartments, condos, and shared homes where water, theft, and liability claims are among the more practical everyday risks.

One more thing gets missed: landlord insurance does not usually protect your own belongings. If the building owner fixed the wall after a fire or pipe break, that does not mean your furniture, clothing, laptop, and hotel stay are automatically handled. Your policy is the layer meant to address your side of the loss, but only if the right coverage is there.

What July updates may actually change, and what may not

Most renters will not see a dramatic policy rewrite overnight, but pricing, availability, and optional protections may still shift enough to justify a review.

State insurance movement often changes the shopping environment first, while the fine print of your own policy still depends on the carrier, form, and endorsements you chose.

This is where headlines can confuse people. A state action, rate filing, or insurance-market dispute does not automatically mean your policy suddenly got stronger. In many cases, what changes first is cost or carrier behavior. Some insurers become more selective. Some raise rates. Some tighten underwriting around claims history, property condition, or local risk. Others may keep a lower premium but narrow optional protections or offer less generous default limits.

California’s recent insurance developments are a good example of a market story that matters to shoppers without guaranteeing a better policy form for renters. The state’s insurance department described the March 2026 agreement involving State Farm as part of a broader effort to stabilize conditions. For renters, the takeaway is practical: if availability or pricing is changing in your state, compare policy details more carefully instead of assuming every quote reflects the same protection.

Meanwhile, not every item in the search results points directly to renters coverage. Vermont’s July 1 insurance law update involving captives and risk retention groups is a real insurance development, but it is not the kind of consumer-facing renters coverage fix that most households should expect to change their apartment policy this month. That distinction matters. Not every insurance headline means a renter should expect better theft, water, or liability protection.

So what might change for a regular renter in July?

- Quote prices may rise or fall depending on your ZIP code and carrier appetite.

- Deductible choices may change, affecting how much cash you need after a loss.

- Optional add-ons such as identity theft, scheduled property, or backup coverage may vary more between carriers.

- Availability may tighten in some markets even if the headline issue sounds unrelated to renters.

The useful move is to treat July as a checkpoint, not a promise. Check what your carrier changed at renewal, what competitors now offer, and whether your state insurance department has posted any consumer guidance that affects shopping conditions where you live.

How to compare policies without getting fooled by a cheap premium

The best renters policy for your budget is usually the one that protects the losses most likely to disrupt your life, not simply the one with the lowest monthly number.

A lower premium can still be the more expensive choice if the deductible is too high or the policy leaves your most realistic risks only partly covered.

Many renters can lower costs and improve protection at the same time, but only if the comparison is honest. Start with apples-to-apples quotes. If one insurer shows a much lower price, check whether the personal property limit, liability amount, and deductible quietly changed. Also review whether replacement cost coverage is included for belongings or whether the policy pays actual cash value, which can reduce what you receive for older items.

A solid quote comparison should include:

- Personal property limit

- Deductible amount

- Liability limit

- Loss-of-use or additional living expense coverage

- Replacement cost versus actual cash value for belongings

- Optional endorsements for high-value or higher-risk items

Cost context helps here. Reviews of 2026 renters insurance pricing suggest renters insurance is still relatively inexpensive compared with many other forms of coverage, but that does not mean every policy is a bargain. A small monthly difference can buy a much stronger liability limit or better replacement terms. For a renter with a dog, a bike, a remote-work setup, or expensive electronics, those upgrades may matter more than trimming a few dollars from the premium.

It also helps to ask about discounts carefully. Bundling with auto insurance can help in some cases, but do not let a bundle hide a weak renters form. Autopay, claims-free history, alarms, and paperless billing may also lower cost. If you are price-sensitive, raising the deductible modestly can reduce premiums, but only if you keep enough cash set aside to actually use the policy when something goes wrong.

Renters with very tight budgets should not assume the answer is to go without coverage. Sometimes the smarter move is to carry a smaller but usable policy, then strengthen the most realistic weak spot with one endorsement rather than overspending on extras you do not need.

What to do this week if your current coverage feels flimsy

A short policy check now can help you find out whether a small update would protect you better before the next claim, move, or renewal notice.

Midyear insurance review works best when you focus on likely losses in your own apartment life, not on abstract disaster scenarios you may never face.

Keep the next steps simple. First, grab your declarations page and your latest bill. Second, list the three losses that would hurt your household most: stolen electronics, water damage to belongings, being forced out of the unit for repairs, or a liability claim after a guest is injured. Third, check whether your current policy would handle those situations well enough.

Then take action in this order:

- Verify your property limit and deductible.

- Check exclusions and category caps for valuables.

- Review temporary housing coverage and liability limits.

- Ask your insurer what optional endorsements are available.

- Get at least two competing quotes with matching limits.

- Check your state insurance department site for consumer guidance if the local market feels unstable or hard to shop.

If you are moving soon, this review matters even more. A new building, neighborhood, roommate setup, or work-from-home arrangement can change what kind of renters protection makes sense. The cheapest old policy may no longer fit your current risk at all.

July does not guarantee that weak renters insurance gaps are finally getting fixed everywhere. In many places, they are not disappearing on their own. But a quick review can still reveal better options, stronger endorsements, or a smarter price for the coverage you actually need. Check what your current policy would really do, compare what other insurers are offering, and see which protections may fit your apartment and budget today.